Home >

Doc >

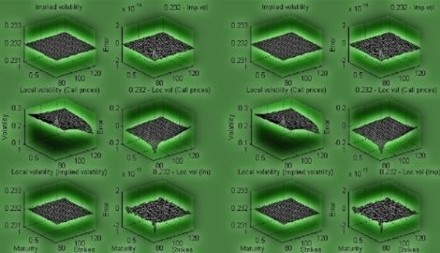

Comparison and problems using local, implied and stochastic volatility obtained from market data to price exotic options

We can estimate the market view using the volatility which is implied by the market prices. Using real data from the market, we can simulate the asset

By Prof. Klaus Erich Schmitz Abe http://www.maths.ox.ac.uk/~schmitz/

Download Excel version: market_september.xls

Download Matlab version: market_september.mat

A complete zip package that contains the matlab files to plot and simulate project: market_plot.zip

Summary: