Home >

Doc >

Global Equity Strategy Part man, part monkey >

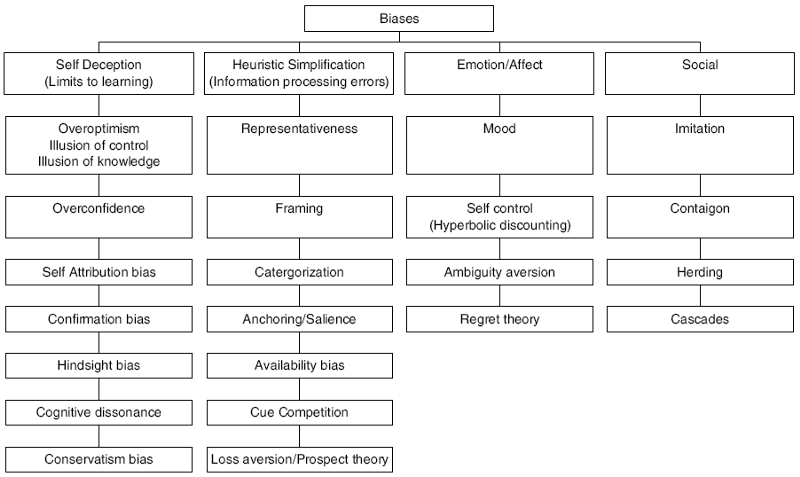

Table of types of errors to which we are prone

The simple truth is that we make mistakes when we come to decisions. Psychologists have spent years documenting and cataloguing the types of errors to which we are prone. The main results are surprisingly universal across cultures and countries. Hirschleifer[1] suggests that most of these mistakes can be traced to four common causes:

- self deception, heuristic simplification, emotion, and social interaction. The table below tries to classify the major biases along these lines. The table outlines the most common of the various biases that have been found, and also tries to highlight only those with direct implications for investment.

{kind=link}

The ten guidelines listed on the front cover try to suggest ways in which we can avoid some of the most perilous of these errors. Simply being aware of their existence is not enough. We need to take active steps to structure our thought process in such a way that it becomes hard to fall back into old habits. Economists frequently assume that people will learn from their past mistakes. Psychologists find that learning itself is a tricky process. Many of the self-deception biases tend to limit our ability to learn. For instance, we are prone to attribute good outcomes to our skill, and bad outcomes to the luck of the draw. This is self attribution bias. When we suffer such a bias, we are not going to learn from our mistakes, simply because we don’t see them as our mistakes.

The two most common biases are over-optimism and over-confidence. For instance, when teachers ask a class who will finish in the top half, on average around 80% of the class think they will! Not only are people overly optimistic, but they are over-confident as well. People are surprised more often than they expect to be. For instance, when you ask people to give a forecast, and provide estimates of 98% confidence intervals, the true answer only lies within the limits around 60-70% of the time!

Over-optimism and over-confidence tend to stem from the illusion of control and the illusion of knowledge. The illusion of knowledge is the tendency for people to believe that the accuracy of their forecasts increases with more information. So dangerous is this misconception that Daniel Boorstin opined “The greatest obstacle to discovery is not ignorance – it is the illusion of knowledge”. The simple truth is that more information is not necessarily better information, it is what you do with it, rather than how much you have that matters.

This leads to the first guideline:(1) You know less than you think you do. The illusion of control refers to people’s belief that they have influence over the outcome of uncontrollable events. For instance, people will pay more for a lottery ticket which contains numbers they choose rather than a random draw of numbers. People are more likely to accept a bet on the toss of a coin before it has been tossed, rather than after it has been tossed and the outcome hidden, as if they could influence the spin of the coin in the air! Information once again plays a role. The more information you have, the more in control you will tend to feel. Over-optimism and overconfidence are a potent combination. They lead you to overestimate your knowledge, understate the risk, and exaggerate your ability to control the situation. This leads to bold forecasts (over-optimism and over-confidence) and timid choices (understate the risk.).

In order to redress these biases (2) Be less certain in your views, aim for timid forecasts and bold choice. People also tend to cling tenaciously to a view or a forecast. Once a position has been stated most people find it very hard to move away from that view. When movement does occur it does so only very slowly. Psychologists call this conservatism bias (it can lead to anchoring which we will discuss a little later). The chart below shows conservatism in analysts’ forecasts. We have taken a linear time trend out of both the operating earnings numbers, and the analysts’ forecasts. A cursory glance at the chart reveals that analysts are exceptionally good at telling you what has just happened. They have invested too heavily in their view, and hence will only change it when presented with indisputable evidence of its falsehood.

1 Hirschleifer, D (2001) Investor Psychology and Asset Pricing, Journal of Finance 56

By Dr James Montier

Next: Market overconfidence

Summary: Index